Block-Chain Technology

Block-chain Technology Explained

The gray man did? The advent of blockchain technology changed the way we view data, transactions and trust. It was first introduced to the public through digital assets like Bitcoin cryptocurrency; blockchain technology has rapidly entered into other fields such as banking, healthcare, real estate and more.

We go where no one else ever goes, we try things that no one actually tries: this is — what I have been doing at Medium for the past two years, in reading about blockchain and cryptocurrency.

What is Blockchain?

A blockchain is a type of database, and all databases store information. At its heart, a blockchain functions as a digital ledger that distributes transactions on computer systems worldwide. A blockchain is a decentralized system, where no single entity (e.g. a bank or government) has control over the entire network. Instead, the ledger is maintained and verified by all participants in the network (the nodes).

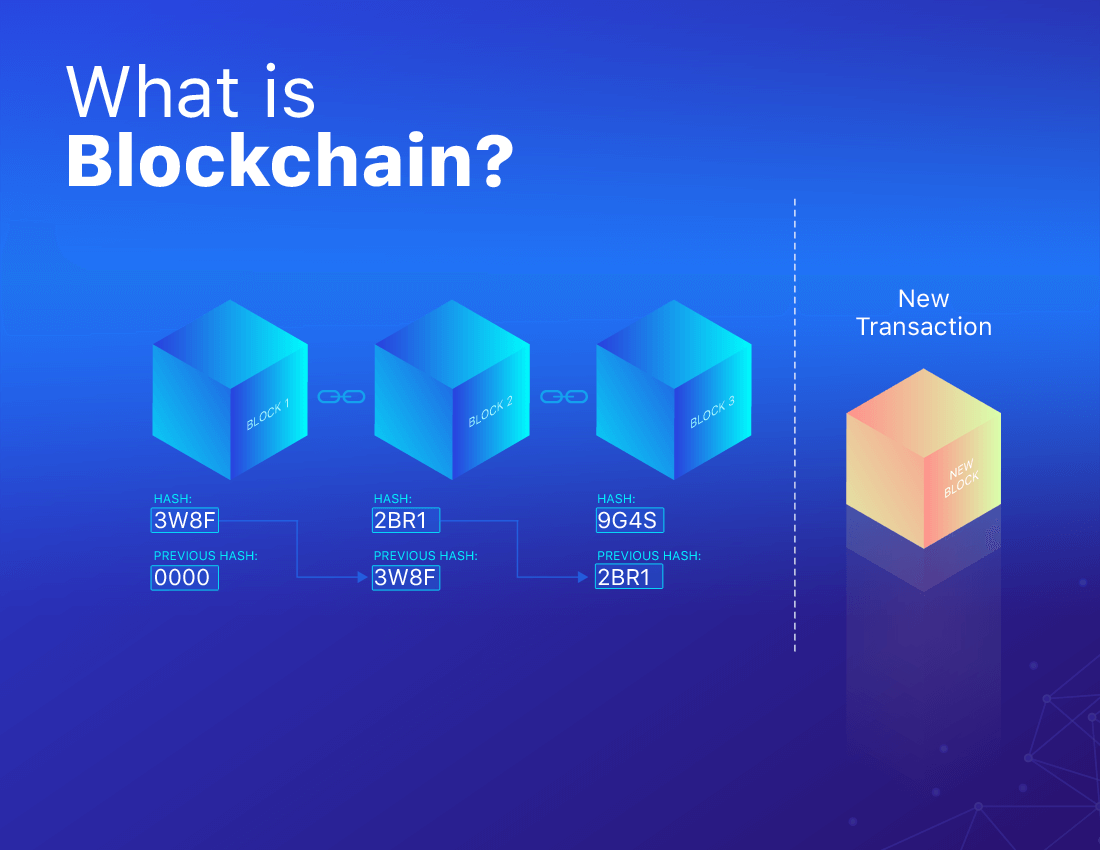

A blockchain is a chain of blocks that contain list of transactions. The blocks are chained together via cryptography, hence the term blockchain. Blocks contain permanent data that, once added is unable to be changed unless you change every block afterwards on the chain. The fact that the ledger is immutable also means this system is tamper-proof and won’t be easily hacked.

The Structure of a Blockchain

Understanding the structure of a blockchain is critical to grasping how it works. There are three key components that make up a blockchain:

Block: A block is a collection of data that is stored in a blockchain. Each block contains three essential elements:

- Data: The information contained in the block, which could be transaction details, contracts, records, etc.

- Hash: A cryptographic fingerprint of the block, unique to that block, ensuring its contents cannot be tampered with.

- Previous Block's Hash: Each block contains the hash of the previous block, creating a link between blocks and forming the blockchain.

Nodes: These are the participants in the blockchain network, each of which holds a copy of the blockchain. When a new transaction occurs, nodes validate it through a consensus mechanism before adding it to the blockchain.

Consensus Mechanism: Blockchain networks rely on consensus algorithms to ensure all participants agree on the state of the blockchain. The two most popular consensus mechanisms are Proof of Work (PoW) and Proof of Stake (PoS).

- Proof of Work (PoW): Used by Bitcoin and several other cryptocurrencies, PoW requires participants (miners) to solve complex mathematical puzzles to validate a transaction and add it to the blockchain. This process is energy-intensive but ensures a high level of security.

- Proof of Stake (PoS): Instead of requiring participants to solve puzzles, PoS relies on participants holding a certain amount of cryptocurrency to propose new blocks. This method is less energy-consuming than PoW and is gaining popularity in newer blockchain networks.

Key Features of Blockchain Technology

Blockchain technology is defined by several characteristics that set it apart from traditional databases and centralized systems. These key features include:

Decentralization: Unlike traditional systems, where a central authority controls data and transactions, blockchain operates on a peer-to-peer network. No single entity has control, making it more resistant to censorship and corruption.

Immutability: Once data is added to the blockchain, it cannot be changed or deleted. This immutability ensures that historical records remain accurate and cannot be tampered with, increasing trust in the system.

Transparency: While blockchain ensures privacy through encryption, it also promotes transparency by allowing participants to view transaction histories. This balance between privacy and transparency makes it an appealing solution for industries like finance and supply chain management.

Security: Blockchain relies on cryptographic techniques to secure transactions and prevent unauthorized access. The decentralized nature of blockchain also reduces the risk of a single point of failure, making it more resistant to hacking.

Efficiency: By removing intermediaries (such as banks or payment processors) and automating transaction validation through smart contracts, blockchain can speed up processes and reduce costs in various industries.

How Does Blockchain Work?

To understand how blockchain works, let’s walk through the basic process of adding a transaction to a blockchain:

Transaction Initiation: A user initiates a transaction. For instance, in the case of Bitcoin, this could be the transfer of a specific amount of cryptocurrency from one user to another.

Broadcast to Network: The transaction is broadcast to the network of nodes (computers) participating in the blockchain. These nodes are responsible for validating the transaction.

Validation: The nodes use the blockchain’s consensus mechanism (either Proof of Work, Proof of Stake, or other methods) to validate the transaction. For example, in a Proof of Work system, miners would compete to solve a cryptographic puzzle to validate the transaction.

Block Creation: Once the transaction is validated, it is grouped with other transactions into a new block. The block is then added to the blockchain in a linear, chronological order.

Permanent Record: The block containing the transaction is now permanently part of the blockchain. The decentralized network of nodes keeps a copy of the updated blockchain, ensuring that all participants agree on its contents.

Types of Blockchains

Blockchains can be categorized into three main types, depending on the use case and the level of access control:

Public Blockchains: These are open and permissionless networks where anyone can participate without restrictions. Bitcoin and Ethereum are prime examples of public blockchains. These blockchains offer high transparency but can be slower due to the need for consensus from a large number of participants.

Private Blockchains: In contrast to public blockchains, private blockchains are restricted to a specific group of participants, often within a single organization. They offer more control and faster transaction times but sacrifice some decentralization and transparency.

Consortium Blockchains: Consortium blockchains are a hybrid model where multiple organizations control the blockchain network. These are commonly used in industries like banking, where a group of institutions might collaborate on a shared, secure ledger.

Real-World Applications of Blockchain Technology

Blockchain’s potential to revolutionize industries stems from its unique features of decentralization, transparency, and security. Here are some real-world applications across various sectors:

Cryptocurrency: The most well-known application of blockchain is in cryptocurrency. Bitcoin, Ethereum, and other cryptocurrencies use blockchain to enable secure, decentralized digital currencies that operate without the need for intermediaries like banks.

Supply Chain Management: Blockchain can enhance transparency and traceability in supply chains. By recording every transaction (from production to delivery) on a shared ledger, businesses can reduce fraud, improve efficiency, and provide consumers with accurate product information.

Finance and Banking: Blockchain technology is transforming the financial industry by enabling faster and cheaper transactions. Traditional systems often rely on intermediaries, such as banks or clearinghouses, to facilitate transactions, leading to delays and additional fees. Blockchain removes the need for intermediaries, streamlining processes like cross-border payments and reducing costs.

Healthcare: Blockchain can provide a secure way to store and share patient records across healthcare providers. By using blockchain, patients can control who has access to their data while ensuring that the records are accurate and tamper-proof.

Real Estate: Blockchain is being used to simplify real estate transactions by providing a transparent and immutable record of property ownership. Smart contracts can automate processes like property transfers, reducing the need for intermediaries like brokers or notaries.

Voting Systems: Blockchain-based voting systems can offer greater security and transparency compared to traditional methods. Votes recorded on a blockchain are immutable, making it nearly impossible to tamper with election results. This technology could increase trust in the voting process and reduce the risk of fraud.

Intellectual Property Protection: Blockchain can help creators of digital content (such as music, art, and literature) protect their intellectual property by providing an immutable record of ownership. This can reduce piracy and ensure that creators receive proper compensation for their work.

Advantages of Blockchain Technology

Enhanced Security: Blockchain uses cryptographic techniques to secure data and ensure that only authorized participants can access it. The decentralized nature of blockchain also reduces the risk of cyberattacks.

Transparency: Transactions on a blockchain are visible to all participants, promoting trust and accountability. This level of transparency can be especially useful in industries like supply chain management and finance.

Cost Efficiency: By eliminating intermediaries, blockchain can reduce transaction costs and speed up processes. For example, cross-border payments using blockchain are often faster and cheaper than traditional methods.

Decentralization: Blockchain eliminates the need for central authorities, reducing the risk of corruption and censorship. This is particularly valuable in areas like finance, where trust in centralized institutions may be low.

Traceability: Blockchain creates a complete, immutable history of transactions, making it easier to trace goods, assets, or records from their origin to their current state.

Challenges of Blockchain Technology

Despite its many advantages, blockchain technology is not without challenges. Some of the key issues include:

Scalability: Public blockchains like Bitcoin and Ethereum can become slow and congested as more transactions are added. Scaling solutions are being developed, but these networks still face performance limitations compared to centralized systems.

Energy Consumption: Proof of Work blockchains, like Bitcoin, require significant energy consumption due to the computational power needed to solve cryptographic puzzles. This has raised concerns about the environmental impact of blockchain technology.

Regulation: Blockchain’s decentralized and anonymous nature can complicate regulatory efforts. Governments are still grappling with how to regulate cryptocurrencies and blockchain-based applications without stifling innovation.

Interoperability:

0 Comments